On 16 May 2024, the UK Government published an implementation update on its development of economy-wide sustainability disclosure requirements (the “Implementation Update“). The Implementation Update, which the UK Government committed to publishing in its 2023 Green Finance Strategy (which you can read more about here), discusses:

- its endorsement of the IFRS Sustainability Disclosure Standards;

- transition plan disclosures;

- the Financial Conduct Authority’s (“FCA“) Sustainability Disclosure Requirements (“SDR“) and investment labels regime;

- the UK Green Taxonomy; and

- nature-related disclosures.

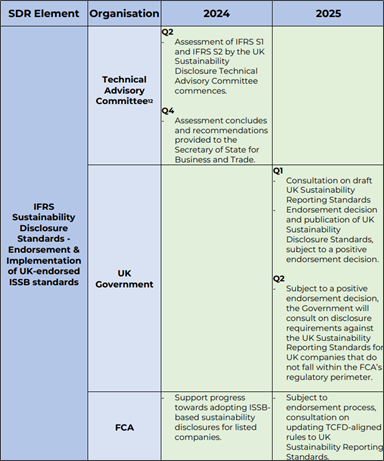

IFRS Sustainability Disclosure Standards

The UK Government has stated that it aims to publish UK-endorsed International Sustainability Standards Board (“ISSB“) Standards in Q1 2025, which (subject to a positive endorsement decision by the UK Government) will be known as the UK Sustainability Reporting Standards. For more information about the ISSB Standards, please read our earlier update here.

The Implementation Update also provides that, subject to a positive endorsement decision by the UK Government, and following a consultation process, the FCA will be able to use the UK Sustainability Reporting Standards to introduce revised requirements for UK-listed companies to report on sustainability-related information. Moreover, subject to a positive endorsement decision, such reporting requirements may then be extended to companies that do not fall with the FCA’s current regulatory perimeter. The UK Government currently expects to make a decision in relation to the above in Q2 2025.

The UK Government has simultaneously published a framework document that sets out further detail about the process and the advisory committees that will support the UK Government in taking these plans forward.

Transition plan disclosures

The Implementation Update provides that the UK Government will consult on strengthening its expectations for transition plan disclosures with reference to the UK Transition Plan Taskforce’s Disclosure Framework in 2025. Further, the UK Government has committed to consulting on how the UK’s largest companies can most effectively disclose their transition plans.

For further information on the UK Transition Plan Taskforce and its Disclosure Framework, please read our earlier updates here and here.

The FCA’s SDRs and investment labels regime

The FCA finalised its SDR and investment label regime, which applies to UK-based funds, in November 2023 (which you can read more about here). The Implementation Update highlights that the FCA has published a consultation, which is open until 14 June 2024, on extending the regime to UK-based portfolio managers. The Implementation Update also highlights that the UK Government intends to issue a consultation in Q3 2024 on whether to broaden the scope of the regime to include funds under the Overseas Funds Regime, regime that allows products of investment funds domiciled overseas to be sold to UK retail investors.

UK Green Taxonomy

The Implementation Updates reiterates the UK Government’s commitment to establishing a UK Green Taxonomy. The Implementation Updates states that the UK Government “continues to work at pace and expects to consult in due course on the proposed UK Green Taxonomy” and suggests that a consultation will take place at some point in 2024.

Once the relevant consultation has been finalised, the UK Government intends to introduce a “testing period” for voluntary disclosures for at least two reporting years before exploring mandating disclosures. Therefore, it is unlikely that a mandatory UK Green Taxonomy will come into effect for at least the next two-three years, if at all.

Nature-related disclosures

The UK Government has welcomed initiatives, such as the Taskforce on Nature-related Financial Disclosures (“TNFD“), and encourages institutions to engage in the TNFD UK National Consultation Group – one of six consultation groups being activated at a national or regional level to expand outreach and engagement on nature-related business and finance – and consider the TNFD recommendations.

For further information on the TNFD, read our earlier update here.

Timeline

The Implementation Update includes the following useful timeline covering the above: